Oklahoma Bar Journal

Modernizing the §1031 Exchange: Leveraging Delaware Statutory Trusts To Serve Clients

By John Newhouse and Ben Newhouse

Internal Revenue Code (IRC) §1031 offers one of the most powerful strategies available to business owners and real estate investors to continue deferring payment of capital gains taxes that would otherwise become due upon the sale of an appreciated asset.[1] Most attorneys who practice in tax or real estate law are generally familiar with the requirements involved in conducting a qualifying §1031 tax-deferred exchange. However, very few such lawyers, as well as only a minority of certified public accountants (CPAs), are aware of how Delaware statutory trusts (DSTs) can also be effectively used to facilitate a fully qualified tax-deferred exchange transaction. Typically, clients engaging in a §1031 exchange transaction simply elect to “swap” one directly owned investment property for another. However, just as the real estate market has evolved, the IRS (via private letter ruling[2]) has also evolved by recognizing and blessing the use of properly structured DSTs to also qualify to receive §1031 tax-deferred exchange treatment.

Internal Revenue Code (IRC) §1031 offers one of the most powerful strategies available to business owners and real estate investors to continue deferring payment of capital gains taxes that would otherwise become due upon the sale of an appreciated asset.[1] Most attorneys who practice in tax or real estate law are generally familiar with the requirements involved in conducting a qualifying §1031 tax-deferred exchange. However, very few such lawyers, as well as only a minority of certified public accountants (CPAs), are aware of how Delaware statutory trusts (DSTs) can also be effectively used to facilitate a fully qualified tax-deferred exchange transaction. Typically, clients engaging in a §1031 exchange transaction simply elect to “swap” one directly owned investment property for another. However, just as the real estate market has evolved, the IRS (via private letter ruling[2]) has also evolved by recognizing and blessing the use of properly structured DSTs to also qualify to receive §1031 tax-deferred exchange treatment.

This article explores the basics of §1031 exchanges, the structure and advantages of DSTs, important legal considerations and best practices for advising clients when considering the use of this modernized vehicle to conduct an exchange transaction.

THE LEGAL FRAMEWORK OF §1031 EXCHANGES

Because the requirements and procedures of §1031 exchanges are well-known and widely understood amongst commercial and real estate attorneys, this article will provide only a brief overview and focus more directly on the often-overlooked role of DSTs in §1031 exchanges. For a more detailed explanation of the requirements involved with §1031 exchanges, the reader is encouraged to review “The Basics of a 1031 Like-Kind Exchange” by J. Max Nowakowski.[3]

Use of a Qualified Intermediary (QI)

Though not explicitly stated within §1031, the exchanging party cannot take actual or constructive receipt of the exchange proceeds upon closing on the sale of the property being relinquished; doing so would violate IRC §1001 and, thus, immediately disqualify the exchange from obtaining tax deferral.[4] To avoid this fate, the exchanging party uses a QI to take actual or constructive receipt of the exchange proceeds on the taxpayer’s behalf.[5] Thus, it’s important to enlist and coordinate the services of a QI before proceeding to close on the sale of the relinquished property.

DELAWARE STATUTORY TRUSTS

Legal Structure and IRS Acceptance

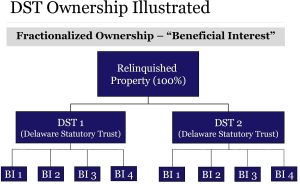

Governed by the Delaware Statutory Trust Act, DSTs are trust entities that allow numerous investors to possess fractional shares in real property through beneficial ownership of the titleholding trust.[6] Investors in a DST are not direct owners of the real estate but instead own an undivided interest in the assets held by the trust, while the DST holds title to the property for the benefit of its many investors.

In 2004, the IRS recognized DSTs’ beneficial interest as qualified/like-kind replacement property for real property relinquished within §1031 exchanges.[7] Via Rev. Rul. 2004-86, the IRS importantly distinguished DSTs from limited partnership (LP) interests for the purpose of §1031 transactions. The IRS further specified that beneficial interests are synonymous with direct ownership interests under §1031, that debt must be allocated pro rata for exchange purposes and that active management must be conducted by the DST and not by its beneficial interest holders.[8] Consequently, this revenue ruling effectively made it possible for taxpayers to conduct a qualifying §1031 exchange transaction in a manner that incorporates passive management strategies of the replacement property. In other words, the taxpayer is no longer relegated to being actively involved in the continual management of their replacement property (as was customary practice with most §1031 exchanges), should they instead prefer to take a more passive role while still retaining/enjoying the tax benefits of owning such directly held real estate interests.

IRS DST Parameters: ‘Seven Deadly Sins’

While Rev. Rul. 2004-86 effectively opened the §1031 door to DSTs, the IRS tempered its acceptance of using such structured vehicles within the private letter ruling by requiring DSTs to be limited in the actions they may take. As such, DSTs:

- May not obtain additional capital

- May not acquire additional debt or refinance current debt

- May not reinvest any subsequent sale proceeds

- May not make capital expenditures; it is limited to making normal repair and maintenance expenses

- May not enter into new leases or *renegotiate existing leases[9]

- May not invest cash between distribution dates to its beneficial owners in anything other than short-term securities

- Must distribute all cash (other than necessary reserves) on a current consistent basis

To deal with these limitations, DSTs tend to contain provisions for springing into an LLC taxed as a partnership (commonly known as a “Springing LLC”) if action prohibited by the IRS within the DST format is needed. While this action is normally not taxable, it does run the risk of limiting future §1031 exit options.

Tenants, Toilets and Trash: DSTs and Passive Management

Among seasoned real estate investors, the burdens of active property management are often summarized – somewhat tongue-in-cheek – by the well-known phrase “tenants, toilets and trash.” This trinity of persistent frustrations often causes once-eager real estate investors to begin searching for viable exit ramps as they face the day-to-day oversight of active property operations and management. The operational realities of being a landlord often detract from the financial rewards, particularly as investors age or desire a more hands-off approach.

The first of these challenges, tenants, requires continuous attention: screening applicants; collecting rent; supervising the property to prevent or mitigate misuse, neglect or damage; or engaging in the eviction process.

Toilets, a stand-in for the broader category of property maintenance issues, are the ever-constant reminder that physical structures require upkeep. Unfortunately, that sometimes means plumbing issues arising at 3 a.m. requiring immediate attention, which threaten not only the profitability of the investment but also the ability to preserve the value of the investment itself.

Trash refers to the physical deterioration and cleanup that often follows tenant turnover. Whether that’s fumigating a rental house where the previous tenant was a smoker, removing abandoned property, repairing damages or repainting walls, the task of keeping the property marketable for future tenants can quickly erode both the net income and the patience of the real estate investor.

DSTs enable real estate investors to move from active management to passive management. Because the DST is a passive real estate investment vehicle, the purchase, financing, management and eventual sale of the property is the responsibility of the DST sponsor to perform – not the investor. Thus, the investor can continue to enjoy the benefits of owning real property without the hassle of day-to-day management.

... And the Other ‘T’: Taxes

Given these cumulative challenges, many long-term real estate investors eventually desire an exit ramp that might enable them to reallocate the value of their investment into other areas, provided such can be accomplished in a tax-efficient (or tax-neutral) manner. However, they are often quickly disabused of that notion by their attorneys and CPAs, who correctly proclaim that a nonstrategic exit from this real estate arena will likely trigger very material tax consequences. If the advisor explains the §1031 exchange process but neglects to include the DST option for consideration, then the investor can be left with the false impression that they can be relegated to a lateral investment move (and maybe further additional capital outlay) via exchanging the currently owned property for another physical “like-kind” property. Thus, the investor becomes at risk of wrongfully concluding that their only effective option is to “trade one problem for another.” Conversely, DSTs can provide the investor with an option that can materially change their current investment situation, while doing so in a tax-neutral manner.

Those investors who entirely disregard the §1031 option run the risk of not only having their transaction be subject to federal and state taxes for capital gains but also two additional taxes: the depreciation recapture tax[10] (DRT) and the net investment income tax (NIIT) of the Affordable Care Act (ACA).[11] Consequently, it is not uncommon for an investor to be forced to cede the majority of their sales proceeds to paying various tax liabilities if a transaction is not properly structured to incorporate the tax benefits of §1031.

DRT is perhaps the most often overlooked and financially significant component in the sale of real estate. Real estate investors typically depreciate the structure (but not the land) of rental income-producing property over a 27.5-year or 39-year schedule.[12] [13] When the real property is sold, the IRS “recaptures” that depreciated amount via a flat 25% tax rate.

A lesser-known but increasingly relevant component of the overall tax burden is the 3.8% NIIT imposed by the ACA. This surtax applies to net investment income, including capital gains, for taxpayers whose modified adjusted gross income (MAGI) exceeds certain thresholds: $250,000 for married couples filing jointly and $200,000 for single filers. The 3.8% tax is applied to the lesser of the taxpayer’s net investment income or the amount by which their MAGI exceeds the threshold.[14] [15]

Suppose a married couple filing jointly has $450,000 in MAGI and $700,000 in capital gains from selling three rental properties. Since their MAGI exceeds $250,000 by $200,000 ($450,000-$250,000), and their net investment income from the sale of the houses is $700,000, the 3.8% tax is assessed against the lower value ($200,000). This NIIT causes an additional $7,600 in federal tax liability to be incurred by the couple.

Using a DST via a §1031 exchange can defer not only federal and state capital gains taxes but also DRT and NIIT. Moreover, the investor can keep deferring this total tax liability into future DSTs (or return to direct ownership) until they die. At death, the investor’s beneficiary is still entitled to receive a step-up in the cost basis of the investment, thereby significantly mitigating (if not entirely eliminating) this overall deferred tax liability while still permitting the investor to enjoy the tax benefits of a real estate investment during their lifetime.

Additional Advantages of Using DSTs in §1031 Exchanges

For real estate investors desiring to transition away from active management, better diversify their real estate holdings or streamline their estate and tax planning, DSTs can offer unique strategic advantages over the options typically used for real property replacement. DSTs offer the following potential advantages.

Access to institutional-quality real estate. The multitrillion-dollar U.S. commercial property market may be a challenge to navigate for individual investors. Partnering with a respected DST sponsor with local market knowledge, who has access to institutional-quality properties coupled with expertise in management and financing, can help real estate investors expand their options when looking for replacement property. Using this strategy, an investor could potentially exchange their apartment complex interest into a DST that owns a $70 million Amazon distribution center. On their own, the investor would likely never be able to afford or manage such an asset.

Diversification. Financial advisors typically advocate that their clients obtain exposure to various asset classes to reduce overall portfolio risk. DSTs can aid in accomplishing the diversification and risk management objectives by exchanging one particular type of real property for several different types of real estate classifications. DSTs usually have flexible minimum investment amounts, enabling investors to exchange into multiple offerings. DST investments can offer multiple property portfolios across a variety of property types (such as commercial, industrial, multifamily, etc.) as well as broad geographic locations. For example, a real estate investor could exchange their eight rental properties (all held in Tulsa), classified as residential real property, for a DST that holds real property assets in industrial (Garland, Texas), commercial (Miami, Florida) and residential (Nashville, Tennessee), thereby accessing multiple sectors and in different geographic locations.

Nonrecourse debt.[16] When an individual owns a building, they are responsible for repayment of debt if a default occurs. DSTs, however, typically use nonrecourse financing. The sponsor of the program (i.e., trustee) takes on the liability and is responsible for any debt repayment on the property, and while there is always risk involved with owning real estate, nonrecourse financing limits the liability for DST investors.[17] [18] [19] For investors approaching retirement who are looking to sell property to simplify their lives, a DST also helps solve the dilemma of trying to secure a mortgage on a replacement property at a time when the investor’s earned income may become reduced (due to retirement), which might make qualifying to obtain future financing more of a challenge.

Simplified tax reporting (grantor letter). Every tax attorney and CPA dreads the Schedule K-1 form. Not only do they tend to be issued late in the tax season, but they’re very complex and require significant skill and time to process. Most real estate holdings, including securitized real estate, cannot avoid K-1 reporting. However, DSTs can bypass Schedule K-1 and issue a grantor trust letter (GTL) that exhibits the DSTs’ allocable income and expenses. The GTL streamlines the tax filing process as compared to the K-1 form.

Closing efficiency. Investor and DST sponsor transaction costs may be lower due to less lender paperwork. In addition, the DST sponsor arranges financing and manages all due diligence efforts. Often, in a §1031 exchange, when a lender is involved, the lender requires a special purpose entity (SPE) to isolate financial risk on the specific real property. Not only does SPE creation add more time and start eating away at the 180-day rule, but the creation tends to generate more expenses, such as legal fees, for the investor.

Relief from underperforming real estate. After factoring in the true costs of real estate ownership, many investors find they own property that provides little or no net income, but they are still hesitant to sell and be forced to recognize capital gains taxes along with DRT and NIIT. A §1031 exchange using a DST may provide a solution to increase cash flow while deferring any taxable event by replacing the property that is not generating sufficient cash flow with a DST designed to do so.

Estate planning. Some investors prefer a role as an active real estate owner, while their heirs may wish to be passive owners. A DST can be a powerful estate planning tool since DST interests can be divided amongst beneficiaries, leaving each to decide what to do with their own portion, while the basis of the property steps up to fair market value (FMV) upon the original owner’s death.[20] This strategy is very effective for many owners of family farms. Family farm owners are often asset rich and cash poor; they understand the tax liability in selling the farm, and often, they have children who either do not want to take over the farm or cannot get the financing to purchase the farm from the parent that would enable the parent to retire. Not only does the §1031-to-DST strategy solve the exit and retirement problem, but it can also solve the estate distribution problem, as well.

Return to active management. If the investor longs for the days of “tenants, toilets and trash” and wishes to return to actively managing investment real estate, the investor always retains that option. Once the DST liquidates, they can simply use the standard §1031 exchange via like-kind property swap and exit out of the passive management scenario (without incurring capital gain or triggering NIIT or DRT) and instruct the QI to acquire a directly owned real estate interest of their choosing.

Eminent domain, destroyed property and §1033 exchanges. Investment properties that have been subject to eminent domain or destruction (fire, flood, etc.) may be eligible for a §1033 exchange. A §1033 exchange applies when a property is lost through casualty, theft or condemnation and incurs capital gains from the proceeds received to pay for the loss.[21] As in §1031 exchanges, a DST may be a replacement solution for these types of exchanges, too.[22] Similar to a §1031 exchange, if reinvested proceeds meet the requirements for the exchange, then capital gains may be deferred. However, unlike §1031, a §1033 exchange can be utilized by the investor even if the event took place in the past two or three years and even if the investor already took receipt of the proceeds.

Disadvantages of Using DSTs in §1031 Exchanges

While the advantages of DSTs are compelling, there are several significant disadvantages that make the §1031-to-DST exchange an inappropriate investment for many investors. These disadvantages include, but are not limited to, the following.

Illiquidity. Individuals entering the DST need to be fully aware that their beneficial ownership interests are completely illiquid for a period of time. Once the investment is made, the principal cannot generally be returned to the investor until the DST initiates and completes a liquidity event.

Complete absence of public secondary markets for DST interests. Since DST shares are illiquid, a public secondary market does not exist for investors (or others) to buy and sell their shares. However, there is a silver lining associated with this aspect: Since there is no public secondary market, the DST shares are marginally correlated to equity markets. Thus, their value tends to remain constant while traditional shares in equities see greater volatility as they are traded. Investors holding securitized real estate, such as a DST, generally must demonstrate that they have a low need for liquidity. Unfortunately, circumstances sometimes arise that change that dynamic, and when they do, investors in DSTs and other illiquid assets will receive unsolicited, deeply discounted third-party offers for their interests.

Long-term time horizons and holding periods. Typically, DSTs tend to exist between five and seven years before the sponsor will begin to consider initiating any type of liquidation process. During that time, if the DST is successful, it will pay (generally on a monthly basis) its beneficial owners a consistent distribution of the income derived from the underlying property. So an investment property holder using the §1031-to-DST strategy is at the mercy of the DST sponsor as to when they can exit the investment. Conversely, if the investor holds on to their physical property, the investor retains the freedom to sell it at any time they deem beneficial.

Complete lack of investor control. As stated in the previous example, the investor loses decision control when entering the DST. The decision of when to sell the DST is determined by the sponsor. Unlike traditional stocks, there are no voting rights associated with an investor’s beneficial ownership interest. When a DST is sold, the investor can roll over sale proceeds into another DST (e.g., keep kicking the proverbial tax can down the road until death when beneficiaries can receive a step-up in cost basis), exchange the sales proceeds into a new directly held property or cash out and pay taxes.

Fees and costs. DST investments tend to be more expensive than other traditional investments. They also incur relatively high management fees (to pay for the professional team operating it), which eat into the investor’s yield, unless significant tax savings from deferral can be obtained.

Inflexibility of structure. As previously mentioned, DSTs are prohibited from refinancing, making capital improvements or amending/altering the lease terms. Properties held in a DST could fall into dereliction if not properly managed or if minor repairs are futile. Thus, it is imperative to evaluate the operational results and reputation of each DST sponsor to mitigate this risk.

General real estate risks. Just as in holding any physical real property, DST beneficial owners assume the same general and market-related risks of changes in cap rates, variations in occupancy, loss of tenants, loss of principal, rising interest rates, limited liquidity and inflation.

Accredited investor status. Like most private placement and securitized real estate investments of an illiquid nature, DSTs can only accept accredited investors as defined by the Securities and Exchange Commission (SEC).[23] To meet the definition, an investor must have a net worth (excluding the primary residence and personal property) that is $1 million or more (trusts not formed for the specific purpose of acquiring the securities being offered must have total assets greater than $5 million, but this high threshold can be waived for grantor trusts where each trustee meets the individual criteria for being an accredited investor). If the investor fails that net worth test, then the investor can qualify by providing the past two years of tax returns showing at least $200,000 of individual income or $300,000 in joint spousal income. Many investors who possess lower-valued real property, such as rental houses for college students, might find the accredited investor status requirement barring their use of a DST.

Tax law changes. While the §1031 exchange has existed since 1921,[24] it tends to be a candidate for elimination (or is often used as a negotiation tool) during tax policy discussions on Capitol Hill. Even though it is unlikely to be eliminated, it is not immune to substantial changes, such as when the sale of personal property became ineligible for §1031 exchange benefits, as occurred in 2017.[25] The most recent major legislation (the One, Big, Beautiful, Bill Act[26] (OBBBA)) resulted in no changes to §1031, DSTs or the like-kind definition. Further, the OBBBA placed no new limitations, caps or phaseouts on §1031 transactions.[27] Again, while the sun still shines on §1031 exchanges, new legislation can always bring about a sunset.

One Last §1031 Wrinkle – §721 UPREIT Exchange – You Need to Know

The intersection of DST investments, IRC §1031 like-kind exchanges and so-called “UPREIT” transactions presents one of the more sophisticated and consequential tax planning crossroads in modern real estate practice. The ultimate moment of decision arrives when DST sponsors offer investors the opportunity to convert their fractional real estate beneficial interests into operating partnership units (OP units) through a §721 contribution to a real estate investment trust’s (REIT) umbrella partnership.[28] [29] The choice to accept such units carries significant implications for future tax deferral strategies, including the ability – or inability – to execute subsequent §1031 exchanges.

The intersection of DST investments, IRC §1031 like-kind exchanges and so-called “UPREIT” transactions presents one of the more sophisticated and consequential tax planning crossroads in modern real estate practice. The ultimate moment of decision arrives when DST sponsors offer investors the opportunity to convert their fractional real estate beneficial interests into operating partnership units (OP units) through a §721 contribution to a real estate investment trust’s (REIT) umbrella partnership.[28] [29] The choice to accept such units carries significant implications for future tax deferral strategies, including the ability – or inability – to execute subsequent §1031 exchanges.

The §721 UPREIT process is a special issue requiring extensive exploration that may be covered in a future article. What attorneys, CPAs and other advisors need to know about this avenue is that while there is a proper time and place for the §721 UPREIT, when their client enters the UPREIT, they are now in a §1031 dead end where that client can no longer conduct a subsequent §1031 exchange using those particular proceeds. This distinction creates what tax practitioners often describe as a “one-way election.”

Further, when an investor selects the UPREIT option, the OP units become commingled with other REIT properties in the sponsor’s portfolio. While that can positively improve the investor’s diversification, the investor is now forced to invest in other properties they did not select, while also having no ability to decide whether future properties being added to the REIT portfolio are desirable for their situation.

In addition, when the investor converts their DST beneficial ownership interests to OP units, that conversion is not a taxable event. However, when the OP units are sold by the REIT at its liquidation event or when the investor decides to liquidate a portion of their REIT interest, an unavoidable taxable event occurs: The investor must now recognize tax liability on the heretofore deferred capital gains, DRT and NIIT.

One of the advantages that’s often expressed when advising a client to accept the §721 UPREIT option is the limited liquidity feature of the REIT in comparison to the essentially nonexistent liquidity aspect inherent in DSTs. Like DSTs, REITs generally are not publicly traded, so they do not offer a secondary market sale option. Instead, the REIT sponsor tends to offer a share repurchase program (SRP) where the sponsor offers shareholders a stated share price for a limited number of shares to be redeemed. However, even with REITS that market this SRP feature, this particular liquidity provision is almost always limited and never guaranteed (and it is not uncommon for the REIT sponsor to suspend or terminate the SRP).

Again, a full discussion of the tax and transactional consequences of IRC §721 is beyond the scope of this article. The aim here is only to caution the reader that converting DST interests into OP units effectively closes the door to conducting future §1031 exchanges for that real estate asset. That does not mean such transactions should be dismissed out of hand. For some investors, the opportunity to more broadly diversify their holdings, gain some measure of liquidity and shift the management of their real estate assets to professional institutions can outweigh the disadvantages. These benefits deserve deeper study than space here allows.

CONCLUSION

The §1031-to-DST exchange strategy is not appropriate for all real estate investment holders. However, when properly structured, the DST option provides significant tax and utility advantages for investors and retiring business owners to consider. It can enable such people to exit the active management duties (and accompanying liabilities) intrinsically attached to holding physical real property, while also providing the benefit of a consistent income stream that is marginally correlated to the performance of equity markets.

Although gaining in popularity, this viable strategy continues to be significantly underutilized today due to a lack of option awareness by attorneys, CPAs and other financial professionals. Thus, acquiring a competent understanding of the strategy’s availability, along with its advantages and drawbacks, will empower attorneys to better advance their clients’ interests in securing appropriate tax deferrals, improving asset diversification and accomplishing valuable estate planning objectives.

Authors’ Note: This article is neither an offer to sell nor a solicitation of an offer to buy any security that can only be made by prospectus. Investing in real estate and 1031 exchange replacement properties may not be in the best interest of all investors and may involve significant risks. Investors should understand all fees associated with a particular investment and how those fees could affect overall performance. Neither Diversify, DFPG or its representatives provide tax or legal advice, as such advice can only be provided by a qualified tax or legal professional, whom all investors should consult prior to making any investment decision.

ABOUT THE AUTHORS

John Newhouse is a consultant and attorney for Charis Consulting LLC, where he provides risk management, investment and tax-mitigation strategies. He graduated from the TU College of Law in 2006. In addition to numerous financial securities licenses, he holds the certified divorce financial analyst and accredited investment fiduciary designations. He also serves as an adjunct professor at the TU Collins College of Business, where he teaches entrepreneurial law, employment law and legal environment of business.

John Newhouse is a consultant and attorney for Charis Consulting LLC, where he provides risk management, investment and tax-mitigation strategies. He graduated from the TU College of Law in 2006. In addition to numerous financial securities licenses, he holds the certified divorce financial analyst and accredited investment fiduciary designations. He also serves as an adjunct professor at the TU Collins College of Business, where he teaches entrepreneurial law, employment law and legal environment of business.

Ben Newhouse is the founder of Vineyard Asset Management LLC, a boutique wealth management firm. Mr. Newhouse specializes in applying the use and benefits of various DSTs and private placement investments for clients. He graduated from the TU College of Law in 2000. In addition to holding numerous financial securities licenses, he is a member of the Missouri Bar Association, a certified public accountant licensed with the Missouri State Board of Accountancy, and he holds the personal financial specialist credential. He serves on the Mission University Board of Trustees, where he also teaches business law as an adjunct professor.

Ben Newhouse is the founder of Vineyard Asset Management LLC, a boutique wealth management firm. Mr. Newhouse specializes in applying the use and benefits of various DSTs and private placement investments for clients. He graduated from the TU College of Law in 2000. In addition to holding numerous financial securities licenses, he is a member of the Missouri Bar Association, a certified public accountant licensed with the Missouri State Board of Accountancy, and he holds the personal financial specialist credential. He serves on the Mission University Board of Trustees, where he also teaches business law as an adjunct professor.

ENDNOTES

[1] J. Max Nowakowski, “The Basics of a 1031 Like-Kind Exchange,” 95 OBJ 42 (June 2024).

[2] Rev. Rul. 2004-86, 2004-2 C.B. 191.

[3] J. Max Nowakowski, “The Basics of a 1031 Like-Kind Exchange,” 95 OBJ 42 (June 2024).

[4] I.R.C. §1001(a) (2025).

[5] Treas. Reg. §1.1031(k)-1(g)(4)(i) (as amended in 1991).

[6] Del. Code Ann. tit. 12, §3801 et seq. (2023).

[7] Rev. Rul. 2004-86, 2004-2 C.B. 191. “Holdings: (1) The Delaware Statutory Trust is an investment trust, under §301.7701-4(c), that will be classified as a trust for federal tax purposes. (2) A taxpayer may exchange real property for an interest in the Delaware Statutory Trust without recognition of gain or loss under §1031, if the other requirements of §1031 are satisfied.”

[8] Id. “interests in the trust may be qualifying property in a tax-deferred, like-kind exchange if the other requirements for such treatment are satisfied.”

[9] Id. Except in the event of an original tenant bankruptcy or insolvency.

[10] 26 U.S.C. §1250(a); IRS Pub. 544, Sales and Other Dispositions of Assets (2023).

[11] 26 U.S.C. §1411 (2025).

[12] IRS Publication 527, Residential Rental Property §2 (2024).

[13] IRS Publication 946, How to Depreciate Property § “Recovery Periods Under MACRS” (2024).

[14] Net Investment Income Tax, Topic No. 559, Internal Revenue Service; Instructions for Form 8960, 2024.

[15] 26 U.S.C. §1411 (net investment income tax).

[16] Priv. Ltr. Rul. 200521002 (May 27, 2005).

[17] Delaware Statutory Trust Act, 12 Del. C. §3801 et seq.; Rev. Rul. 2004-86.

[18] Instructions for Form 6198 (2024), At-Risk Rules (Treas. Reg. §1.465-27).

[19] 26 C.F.R. §1.465-27 (qualified nonrecourse financing).

[20] I.R.C. §1014(a) (2025).

[21] I.R.C. §1033 (2025).

[22] Private letter ruling (PLR) 200644019 (Nov. 3, 2006). Although not precedent, this PLR allowed a taxpayer to use DST interests as replacement property in a §1033 exchange after a condemnation.

[23] 17 C.F.R. §230.501(a) (2025).

[24] Revenue Act of 1921, ch. 136, §202(c), 42 Stat. 227, 230 (1921).

[25] Tax Cuts and Jobs Act, Pub. L. No. 115-97, §13303, 131 Stat. 2054, 2124 (2017).

[26] Public Law 119-21, An Act to provide for reconciliation pursuant to title II of H. Con. Res. 14, 139 Stat. 72 (July 4, 2025).

[27] Evan Liddiard, “‘Big Beautiful’ Tax Bill Now Law: In-Depth Analysis,” Nat’l Ass’n of REALTORS, (July 14, 2025), Big Beautiful Tax Bill Now Law: In-Depth Analysis, NAR, https://bit.ly/47XjOwQ.

[28] 26 U.S.C. §721(a): “No gain or loss shall be recognized to a partnership or to any of its partners in the case of a contribution of property to the partnership in exchange for an interest in the partnership.”

[29] Treas. Reg. §1.721-1(a): confirms that the contributor receives a partnership interest in exchange for the contributed property.

Originally published in the Oklahoma Bar Journal – OBJ 97 No. 5 (May 2026)

Statements or opinions expressed in the Oklahoma Bar Journal are those of the authors and do not necessarily reflect those of the Oklahoma Bar Association, its officers, Board of Governors, Board of Editors or staff.